Fall Rebalance and Market Outlook

The K-Shaped Recovery

By Brian Aberle

Hello Friends,

In early September, I carried out the second of our normal two annual rebalances within our client portfolio models. Though most of our clients likely saw relatively minor adjustments as most holdings were within their allotted range, we did make a few tactical adjustments both on the stock and bond market side within most portfolios. More information on said adjustments is below. Markets these days seem more fluid than they've ever been (either that, or I'm old; don't answer that), so further adjustments may be warranted, as I reserve the right to change my mind.

In this communication, I provide a summary of my thoughts on the economy, financial markets and portfolio positioning. For those seeking a bit (a lot?) more context, I've provided a much deeper dive into my thinking as part of my video that you can access here or by clicking on the image of the K above the title. Once the video loads, I've created chapters below to help you with navigation.

Rebalance Executive Summary

Within the stock market elements of our portfolio models, my thematic view of the global economy and markets has not changed much. I continued to believe that the U.S. economy will experience a soft landing (some weakness but not recession) to no landing (continued economic growth). Therefore, I made only subtle changes within the tactical slice of our client portfolios, opting to reduce exposure to U.S. "quality" based stock strategies (JQUAL, XMHQ) in favor of more exposure to an equally weighted S&P500 instrument (RSP) and International Quality (IQLT) where I felt appropriate.

I also added short-term tactical exposure to an equally weighted U.S. Healthcare ETF (RSPH) in models 4 and up on the risk scale. Healthcare is often seen as more of a defensive sector of the U.S. economy, and aside from the leading GLP-1 weight loss darlings that are trading at A.I. valuations, the sector seems reasonably priced, particularly if we see more of a broad slowdown in the economy. More on this is in the video and below.

Within bond elements of most portfolios, I opted to go against the market grain somewhat, opting to reduce or eliminate (in more aggressive portfolios) exposure to short-term bonds (Tickers BSV or SUB) in favor of ultra-short-term instruments (JPST, JA) and emerging market debt (VWOB). 2 to 5 year Treasury bond yields have come down much more than 1-year or shorter bonds.

The Treasury markets have reacted over the past few months as if inflation is collapsing (deflation risk?) or the economy will experience Financial Crisis levels. Based on our data, neither of these two events is realistic, as bonds with higher credit risk (junk bonds) have held study.

Finally, I swapped out the Schwab Treasury Obligations Money Market Fund (SNOXX) for the Schwab US Treasury Money Fund (SNSXX). The yields on the two instruments are nearly identical, but SNSXX offers a bit more tax favorability for investors with state income tax.

I believe recession risk over the next six months is low and that rate cut expectations are way overdone. Data suggests that economic growth is still healthy, albeit not at inflation triggering levels like we saw in 2021 and 2022.

Understanding the Purpose of the Rebalance - It's Not for Show

We like to carry out a full rebalance every six months or so. Our rebalance process serves two roles for our clients. First, it helps ensure that our portfolio holdings are within an appropriate range of their respective targets. While we want to allow holdings to drift somewhat (normally 10% to 20% relative) from their target, we don't want them to drift too far. Second, it affords us an opportunity to review our prior investment themes to see if they still hold water or if adjustments need to be made in our thinking.

The thematic work is where the sausage is made, so to speak. I am a sponge for information, utilizing research from nearly any reputable data I can get my hands on, from the biggest investment banks and brokerages out there to the more focused macro, quantitative and sentiment-oriented firms. I also get data from the Federal Reserve, Open Table, the Travel industry, numerous hedge funds and private equity institutions and even social media.

With all of this information often comes investment themes that I can dig into further. The tricky part is then to look at this vast body of opinions and data to help determine an appropriate path forward for our clients, ranging from our most conservative to aggressive. Most of the time, we identify three themes that are most likely to play out, whether good, bad or ugly. Of course, only one can be correct, which assures us a 66% failure rate out of the gates. You are welcome, I guess.

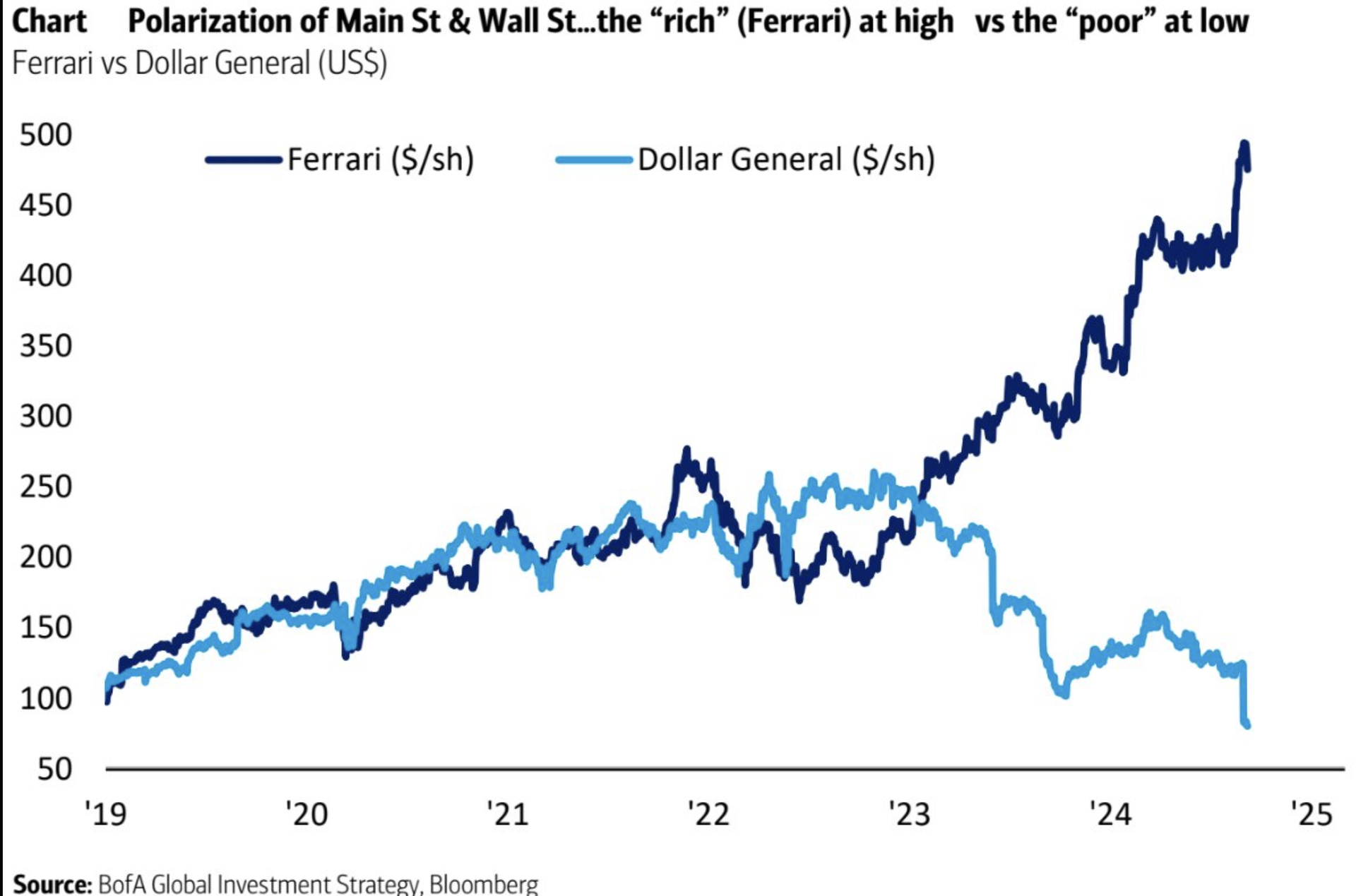

The K-Shaped Economy - In a Picture

As summarized in my video, perhaps nothing illustrates the narrative of a K-shaped economy better than that of Ferrari common stock versus that of Dollar General. For those of us on Wall Street (investors, business owners, etc.), things seem to be "pretty good," while those living paycheck to paycheck most certainly have not enjoyed the past three years as much. Inflation, and the corresponding monetary battle to curtail it via higher interest rates has been painful

Figure 1: Ferrari vs. Dollar General

Source: Bank of America

Figure 1:

Source:

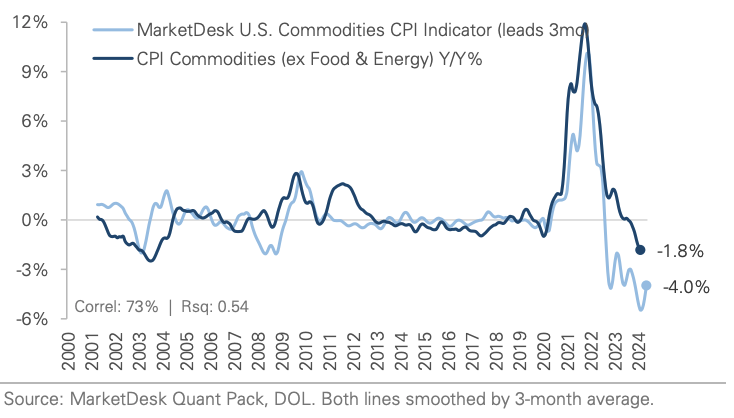

Economic Snapshot - Inflation Continues to Trend Lower

The story of 2022 and 2023 was inflation. Data, however, continues to show that inflation is trending lower. Some economists feared inflation would stay higher for longer (it has been quite stubborn), but evidence suggests the contrary.

Figure 2: Commodities

Source: MarketDesk

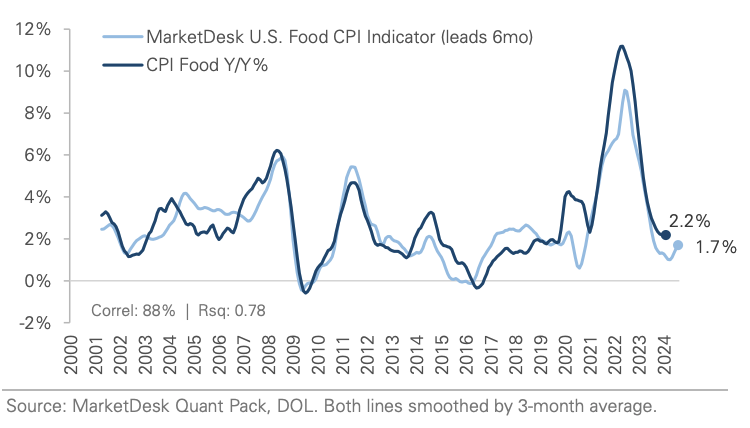

Commodity prices like raw materials (above) peaked in 2022 and are now in a deflationary pattern. Meanwhile, food prices have also shown a noticeable rolling over since the 2022 peak. Shelter and services are still higher than what most would want but also trending down (more in the video on these).

Figure 3: Food Inflation

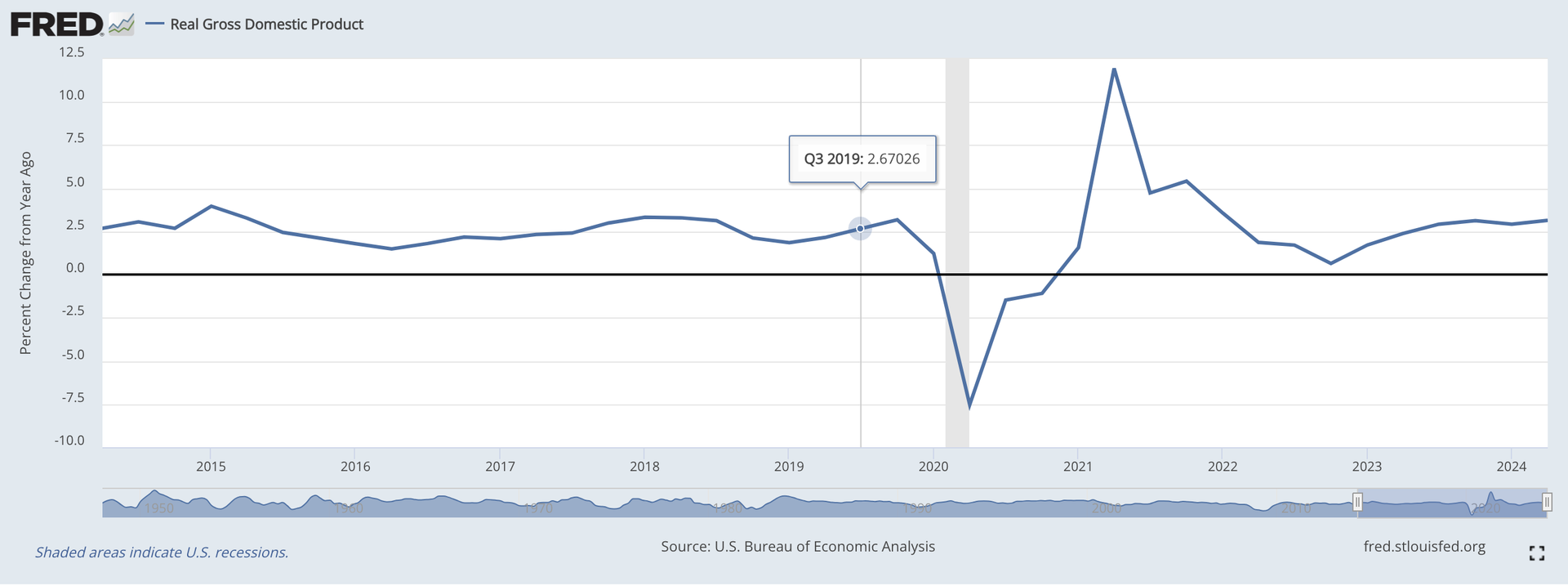

Following the Covid economic collapse and reopening surge, the economy has normalized to around 2-3% growth. As of now, there is little evidence to suggest broad economic weakening.

Figure 4: Economic Growth (GDP)

Source: St. Louis Federal Reserve (Fred.gov)

Following the Covid economic collapse and reopening surge, the economy has normalized to around 2-3% growth. As of now, there is little evidence to suggest broad economic weakening.

Stock Market Review - Bumpy Summer, Rally Since Early August

After a bumpy spring, given fears of a resurgence of inflation, stock markets globally have enjoyed a healthy rally. The biggest winners of 2023 continued their leadership into early 2024, but we've seen a bit of convergence in returns for several months now. Whether this is a blip or the beginning of a broader participation within the stock markets, we'll have to see.

I believe should the economy continue to show signs of strength, a broadening out is warranted. Companies outside of the top 10 or 50 trade at relative discounts to their earnings, while international companies see an even wider discount relative to earnings.

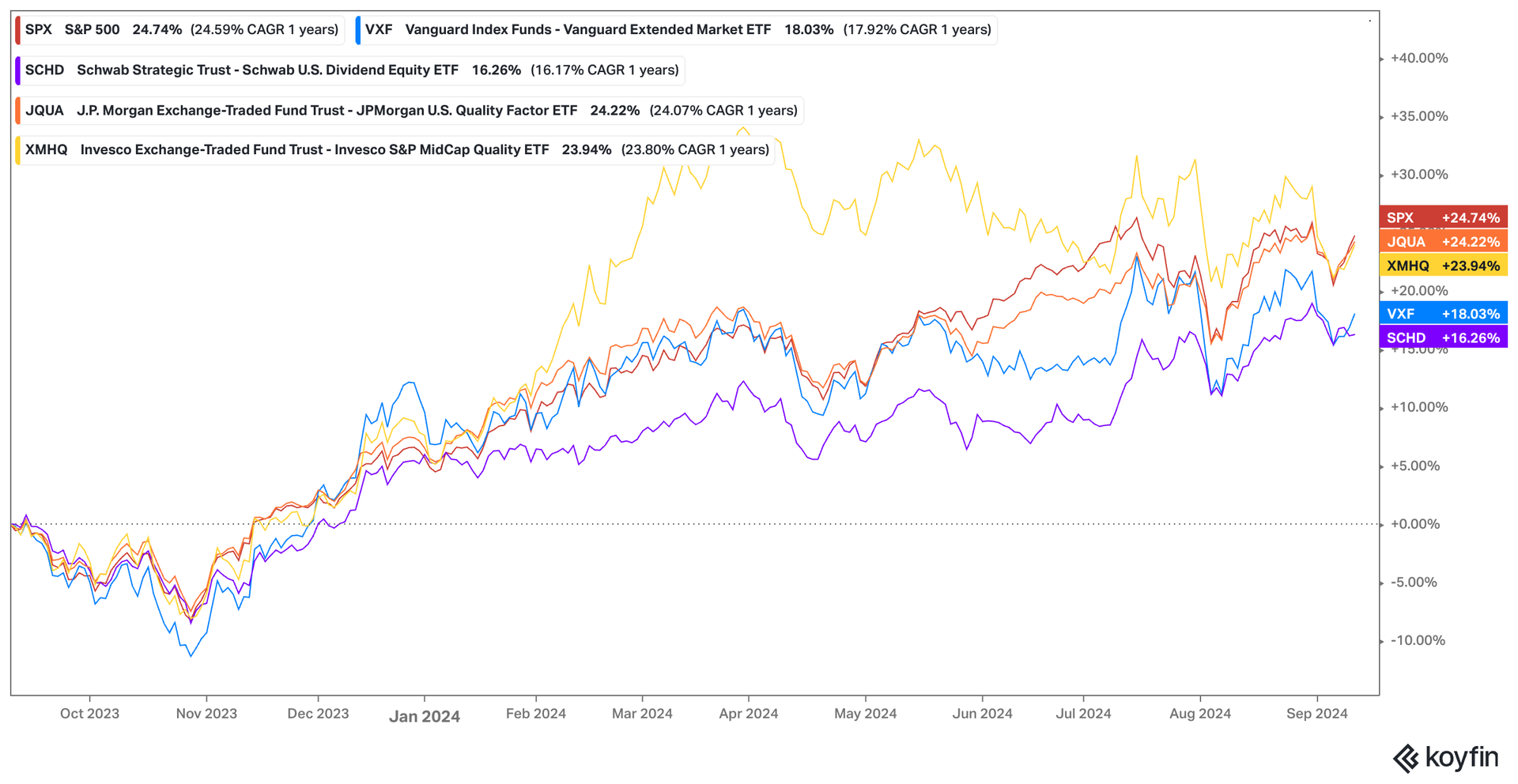

Figure 5: Core and Tactical US Equity Holdings - 1 Year Returns

Source: Koyfin

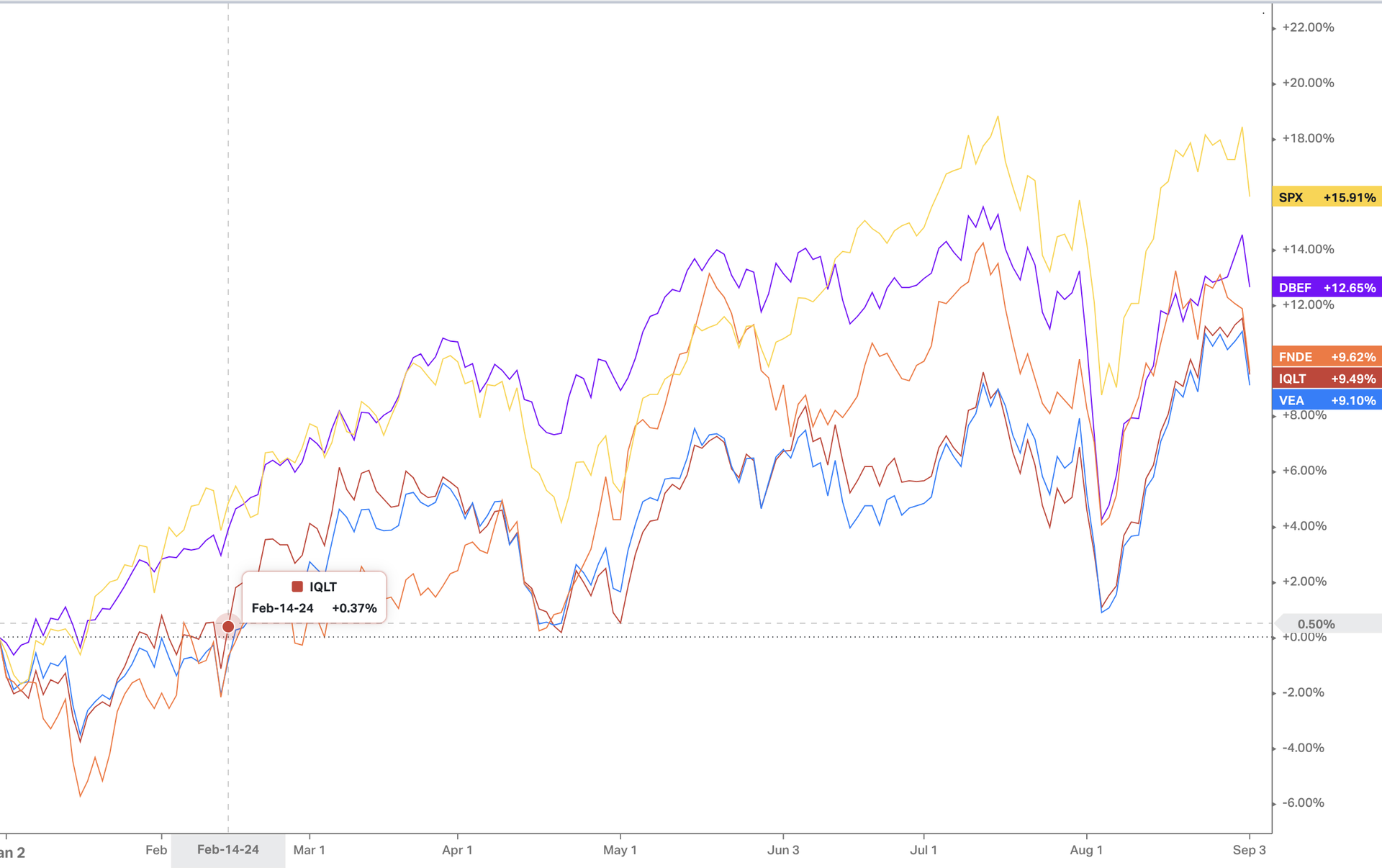

International returns have been quite reasonable, though still lagging the U.S. S&P 500 YTD. Currency hedged equity strategies like with ticker DBEF have kept pace a little better.

Figure 6: International Equities - Good but not Beating U.S.

Source: Koyfin

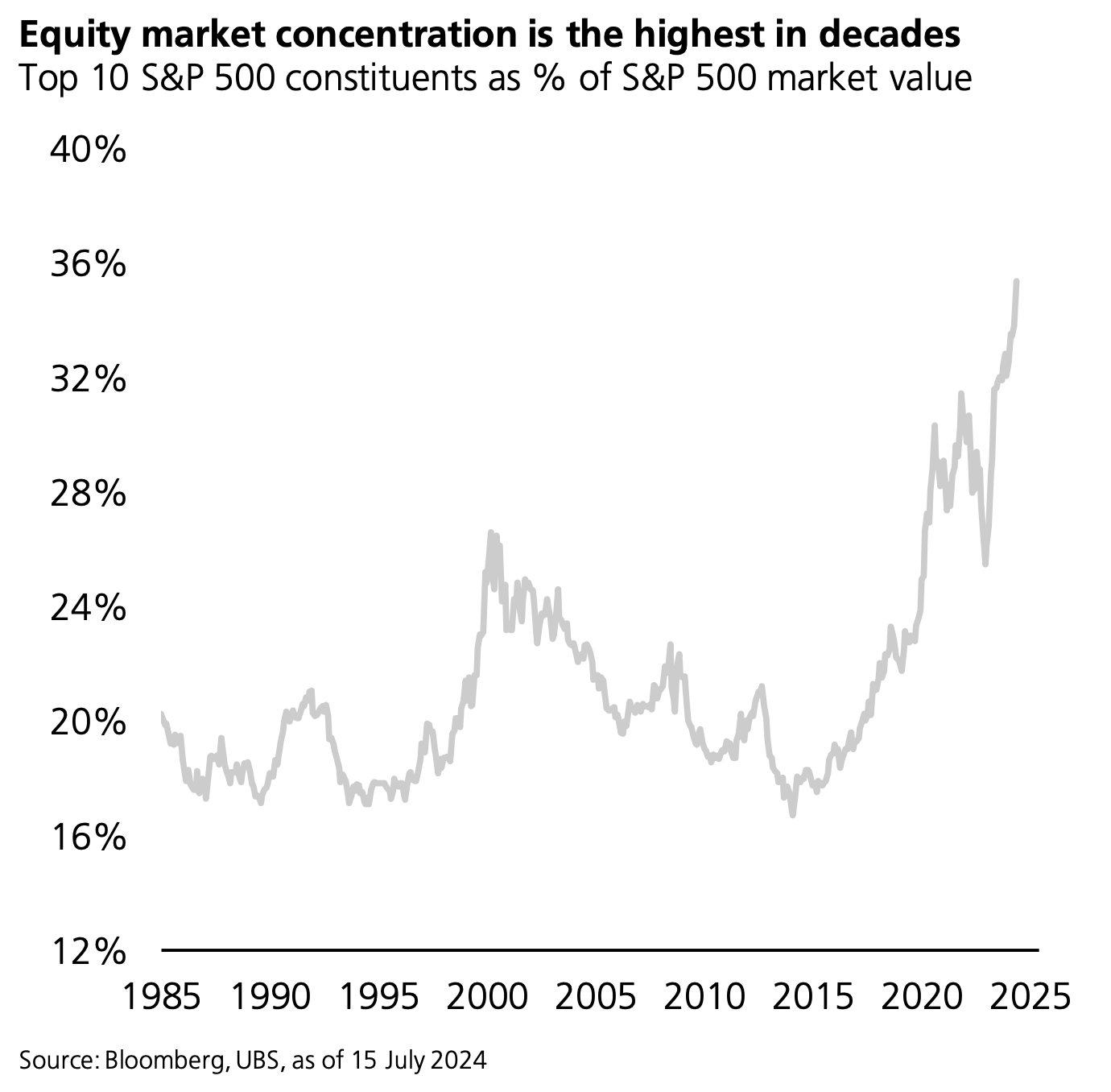

One area investors have been grappling with has been how much the top ten companies in the S&P, mostly technology companies, now represent. At nearly 36%, it is the highest concentration in decades, well exceeding even the dot.com boom of the late 90's.

How might this concentration unwind? Do we need a significant market pullback in time, or will it be something more gradual like we saw post dot.com bust, with other sectors like financials, energy and health care leading the way and thus "catching up"?

I've been in the position for some time that we see a catch-up of small and mid-sized companies. While they haven't done poorly, they just haven't matched the growth of the largest companies, which only enhances this outstretched concentration.

Figure 7: S&P 500 Concentration

Source: UBS

Fixed Income/Bond Review

After a rally in Q4 of 2023, intermediate and long-term bonds once again struggled through April on resurgent inflation fears. However, with inflation now looking more like a downward trend, bond yields have fallen, and prices have moved higher. Instruments with longer maturities (10 years rather than 1 year) have a much greater sensitivity to yields and have thus enjoyed some recovery from the doldrums of 2022 and 2023, two of the worst years for long bonds in centuries... yep.

Instruments with very short maturities, like JA and JSPT, tend to be free of price volatility but will see a great impact in yield from Federal Reserve monetary policy. With the Fed now lowering rates (1/2 a percent on 9/18), the "growth" (income) of short-term bonds will adjust in lockstep.

I believe we are at a fair level for interest rates right now. Even with rate cuts, short-term bonds still offer a competitive yield compared to intermediate or long bonds. Unless you believe a recession is imminent (I do not), we are appropriately positioned. I may entertain a further position in international bonds or instruments like AGG.

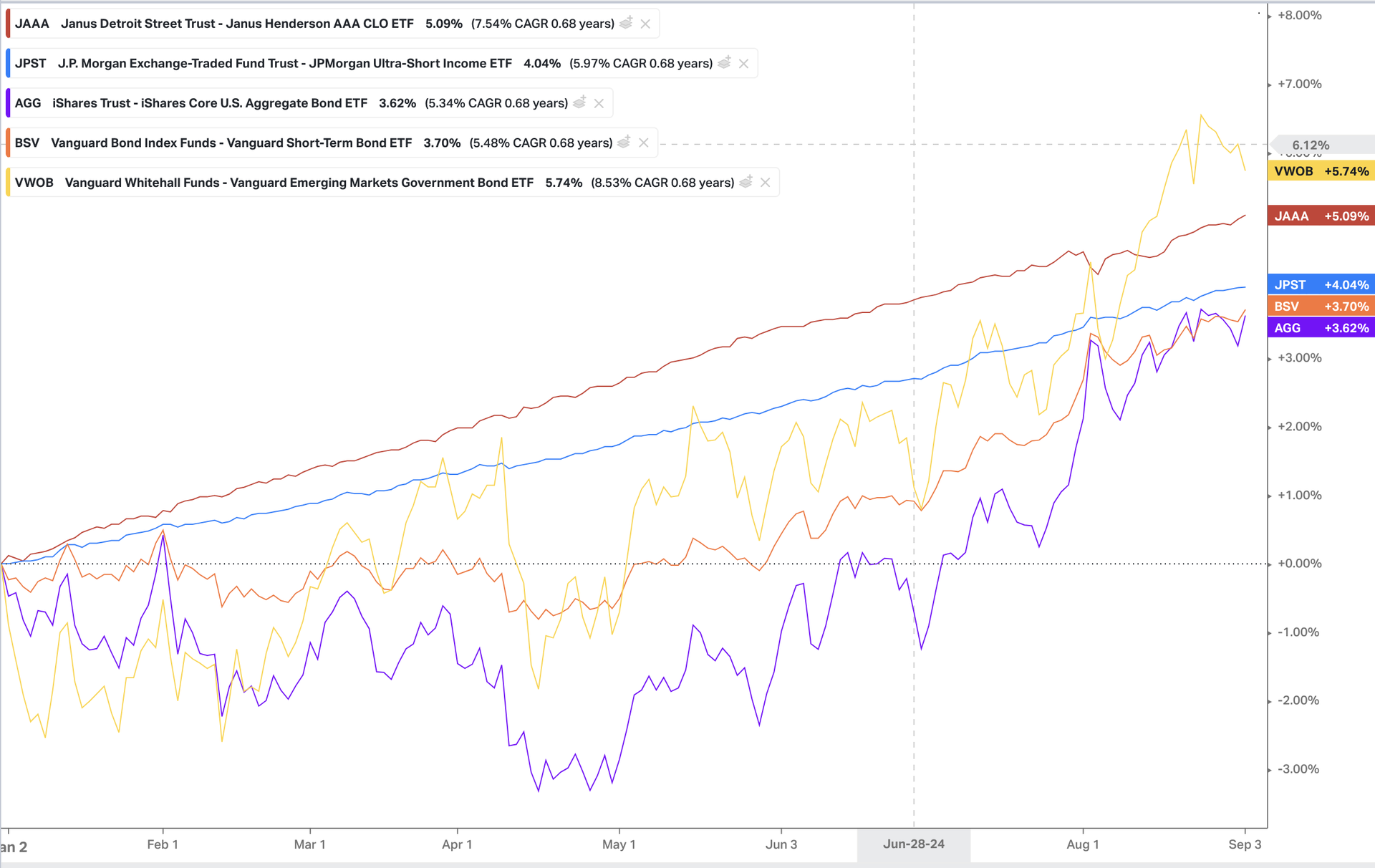

Figure 8: Bond Instrument Returns

Source: Koyfin

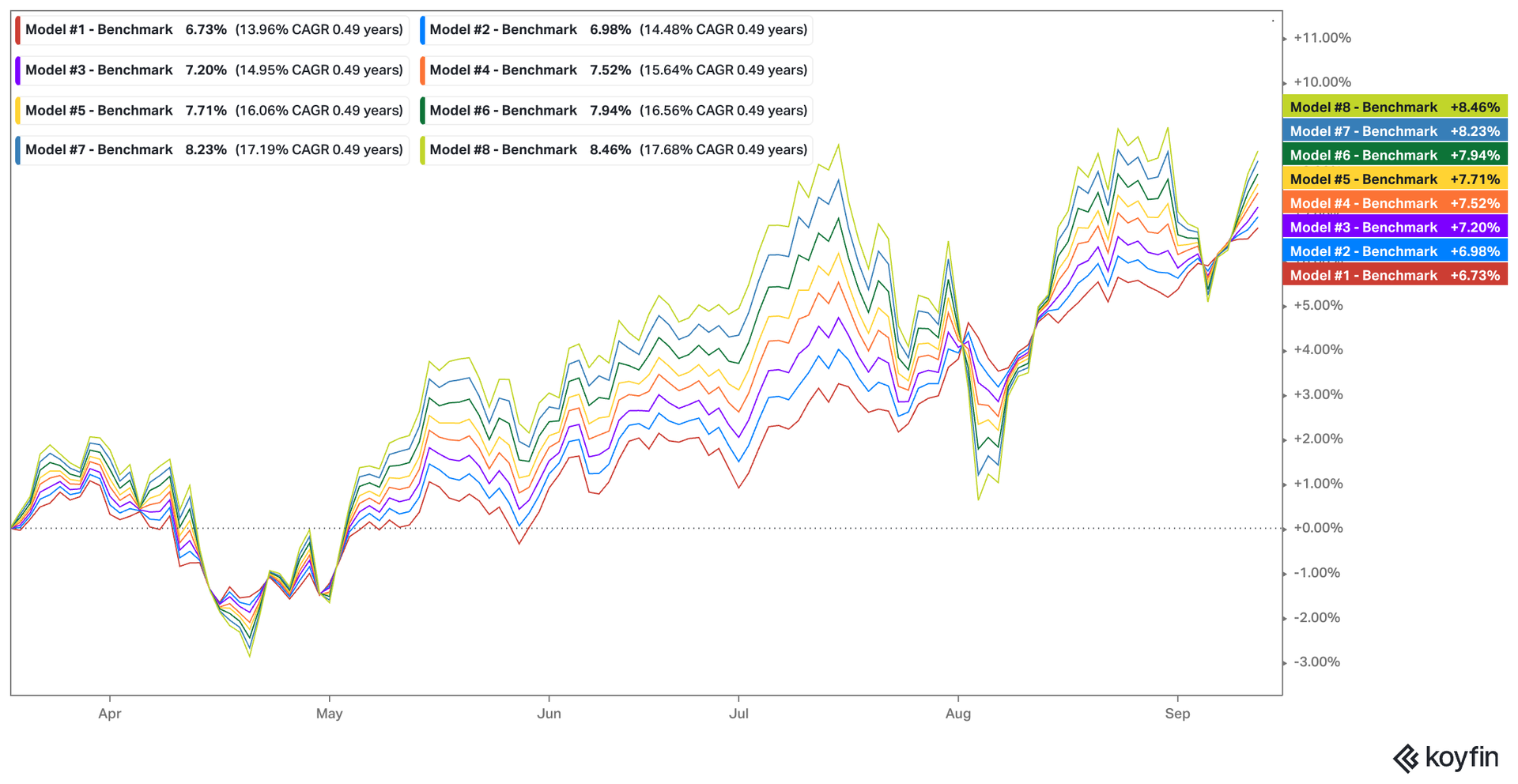

Model Benchmarks - Now Better Participation

With bond yields falling and, thus, bond prices rising, we're seeing a bit more growth in model portfolio benchmarks. Given the contribution of bonds, more conservative model benchmarks have outperformed the more aggressive benchmarks at different times in 2024.

Figure 9: Model Benchmarks - Six Months

Source: Koyfin

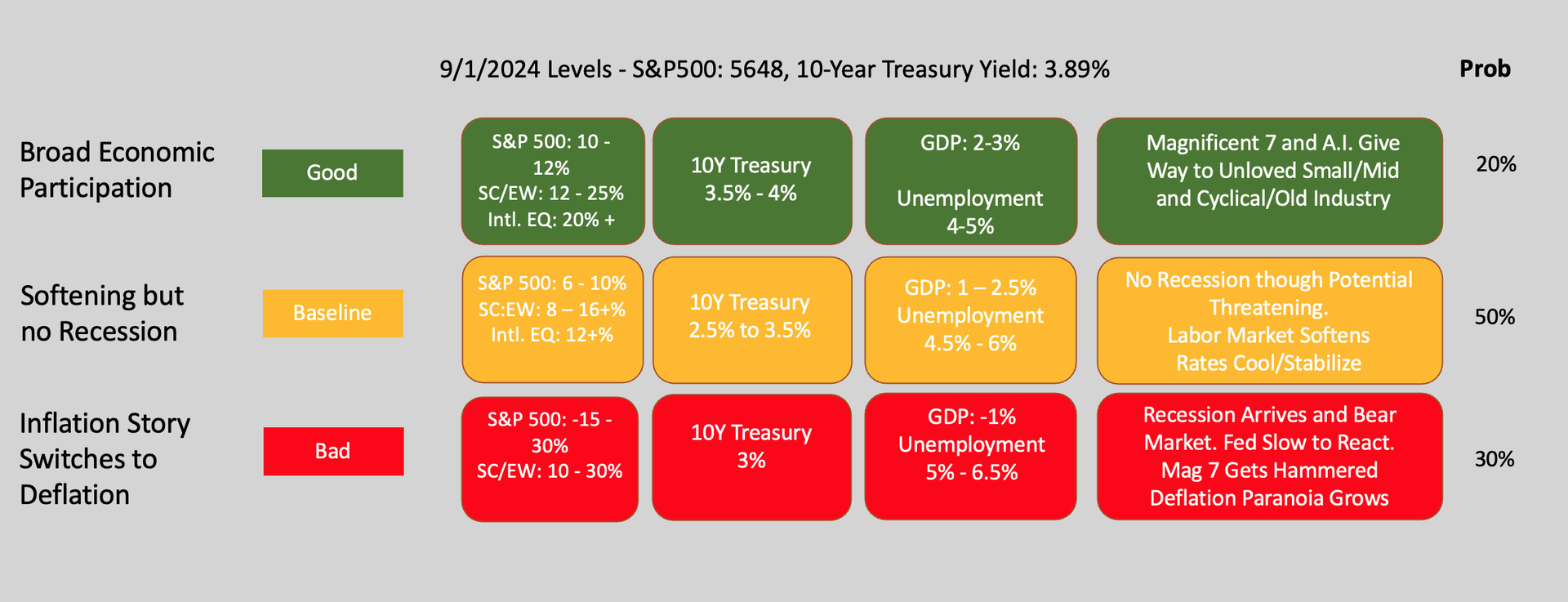

Fall 2024 Themes and Potential Outcomes

As has been the recent custom, I've created three potential scenarios for the next twelve months. I continue to believe that the economy will be resilient with a broadening out of participants showing strength. Mega-sized technology companies still dominate the daily narrative, though, in 2024, utilities, financials, insurance companies and real estate are performing better.

Should a broadening out continue, as we saw following the dot.com bust in the early 2000s, instruments like equal weight small and mid-cap and perhaps international (if the global economy strengthens) will outperform.

My baseline is for a potential economic softening but no recession, the classic soft landing approach. I lean somewhat toward an economy that is at much "risk" of strengthening as it is weakening, however. I believe upper single-digit returns for the S&P 500, along with potentially higher returns for those "broadening" participants, is possible.

I don't expect many fireworks within fixed income, barring an outright economic deterioration or geopolitical event (terrorist attack, war, etc). It's hard to see intermediate Treasury bonds falling much further from current levels. Short-term Treasuries may have more room to go, given changes to Federal Reserve policy.

My "bad" scenario, which I put at just 30%, would be a recession and a possible new narrative of deflation. While nobody likes to see prices on goods and services jump, data suggests some deflationary pressure is starting to creep in with respect to commodities and energy. Deflation would help bring prices down, but not without some more serious economic challenges, such as rising unemployment and stock market volatility. "I wish prices would come back down" is one of those "careful what you wish for" events that is often a challenge for all.

Figure 10:

Source: Aberle Investment Management

Thank you, as always, for the opportunity you give us to assist you with your investment management needs.

Unpretentious Wealth Management

in the Rocky Mountains

Contact

Aberle Investment Management LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. Be sure to consult with a qualified financial adviser or tax professional before implementing any strategy discussed herein. Past performance is not indicative of future returns.

This material is prepared by Aberle Investment Management and is not intended to be relied upon as investment advice and is not a recommendation, offer, or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed in this presentation may change as subsequent conditions vary.

The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by Aberle Investment Management to be reliable, are not necessarily all-inclusive, and are not guaranteed accuracy. As such, no warranty of accuracy or reliability is given, and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Aberle Investment Management.

This material may contain ‘forward-looking’ information that is not purely historical. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

This presentation is intended only for clients of Aberle Investment Management.

Securities mentioned within this presentation may or may not be in all client portfolios. Feel free to cross-reference your holdings to this presentation.

Diversification and rebalancing of a portfolio cannot assure a profit or protect against a loss in any given market environment.

Past performance is no guarantee of future results. Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

A decision to invest in any such investment fund or other investment vehicle should not be made based on any of the statements set forth in this document. Prospective investors are advised to make an investment in any such fund or other vehicle only after carefully considering the risks associated with investing in such funds, as detailed in an offering memorandum or similar document that is prepared by or on behalf of the issuer of the investment fund or other vehicle.

Spread is the percentage point difference between yields of various classes of bonds compared to treasury bonds.

A basis point is a unit that is equal to 1/100th of 1%, and is used to denote the change in a financial instrument.

Should you seek additional clarity on a specific slide or current portfolio positioning, please do not hesitate to reach out to Brian Aberle at brian@aberleinv.com